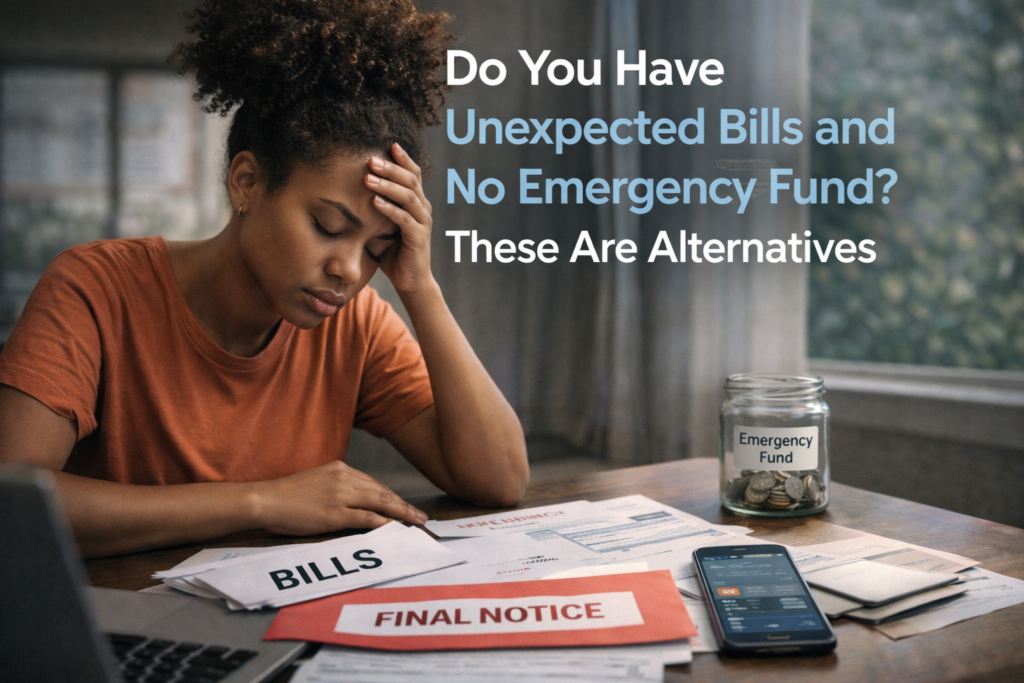

Imagine paying insurance premiums for years, only to discover that your policy doesn’t cover the situation you actually need help with.

Unfortunately, it happens more often than most people think.

Many consumers assume that simply having insurance means they’re protected. In reality, the wrong coverage, outdated policies, and overlooked details can create expensive gaps that leave you responsible for thousands of dollars in unexpected costs.

The good news is that most insurance mistakes are preventable.

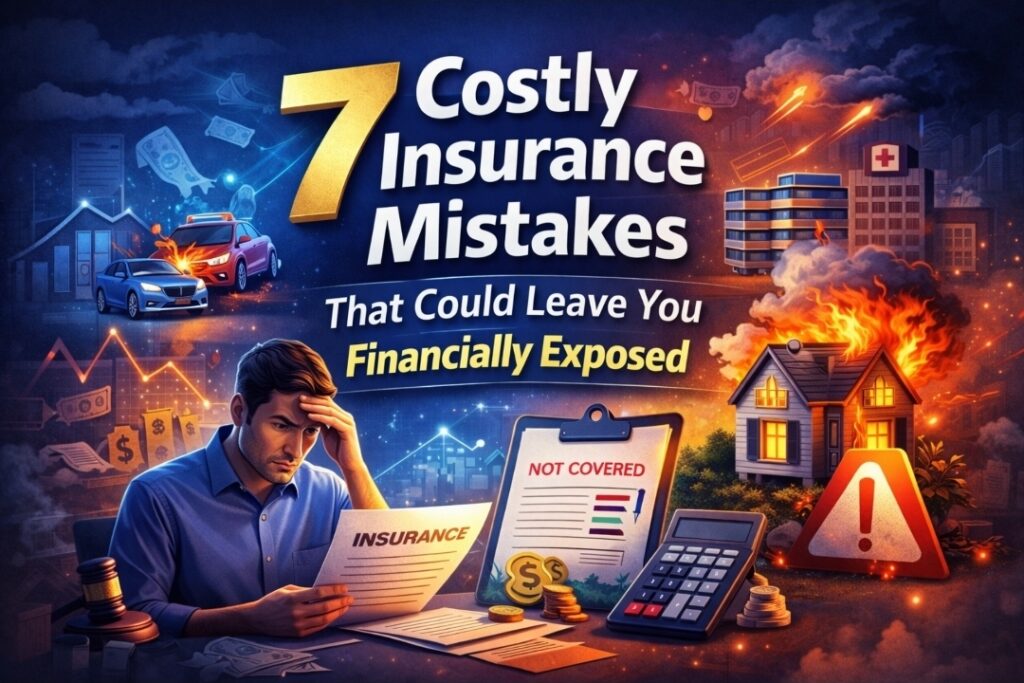

Here are seven costly insurance mistakes to avoid if you want to protect your finances and your future.

1. Choosing the Cheapest Policy Without Reading the Coverage

Everyone wants to save money.

However, selecting an insurance policy based solely on price can be a costly mistake.

A lower premium often means:

- Higher deductibles

- Lower coverage limits

- More exclusions

- Fewer benefits

The cheapest policy isn’t always the best value.

Before purchasing any policy, review what is actually covered and compare benefits not just monthly costs.

Ask Yourself:

“If I had to file a claim tomorrow, would this coverage be enough?”

2. Underinsuring Your Home or Property

Many homeowners underestimate the cost of rebuilding their property after a major loss.

Construction costs, labor expenses, and material prices continue to rise.

If your home is insured for less than its rebuilding cost, you may have to pay the difference out of pocket after a covered loss.

Review your coverage annually to ensure it reflects current replacement costs.

3. Ignoring Life Insurance Until It’s Too Late

One of the biggest misconceptions about life insurance is that it’s only necessary for older adults.

In reality, life insurance is often more affordable when you’re younger and healthier.

If someone depends on your income, life insurance can help protect your family from financial hardship if the unexpected occurs.

Waiting too long can mean:

- Higher premiums

- Health-related exclusions

- Reduced coverage options

4. Failing to Update Beneficiaries

Major life events can quickly make your beneficiary information outdated.

Examples include:

- Marriage

- Divorce

- Having children

- Death of a beneficiary

Many people forget to update their policies after these events.

As a result, benefits may be paid to someone they no longer intended to receive them.

Review beneficiary information at least once a year.

5. Assuming Your Employer’s Insurance Is Enough

Employer-sponsored insurance can be valuable, but it often isn’t sufficient on its own.

Many workplace life insurance policies provide limited coverage that may only equal one or two years of salary.

If you leave your job, coverage may also end.

Consider whether additional individual coverage is necessary to meet your long-term needs.

6. Not Understanding Your Deductible

Many policyholders don’t fully understand how deductibles work until they need to file a claim.

A lower premium often comes with a higher deductible.

Before choosing a policy, ask yourself whether you could comfortably afford the deductible if an emergency occurred tomorrow.

The best policy is one that balances affordable premiums with a deductible you can realistically pay.

7. Never Reviewing Your Insurance Policies

Life changes.

Your insurance coverage should change too.

Unfortunately, many people purchase a policy and never review it again.

You should reassess your coverage whenever you experience major life events such as:

- Buying a home

- Getting married

- Starting a business

- Having children

- Purchasing a vehicle

- Significant income changes

An annual insurance review can help identify gaps and ensure you’re adequately protected.

Quick Insurance Health Check

Ask yourself these questions:

✅ Do I understand exactly what my policy covers?

✅ Are my coverage limits still adequate?

✅ Have I updated my beneficiaries recently?

✅ Could I comfortably afford my deductible?

✅ Have I reviewed my policies within the last 12 months?

If you answered “No” to any of these questions, it may be time to review your coverage.

Compare Insurance Options Before You Renew

One of the easiest ways to potentially save money while improving your coverage is to compare multiple insurance providers before renewing your policy.

Many consumers stay with the same insurer for years without realizing better options may be available.

Comparing quotes can help you:

- Find lower premiums

- Discover better coverage options

- Identify policy gaps

- Improve overall protection

Final Thoughts

Insurance isn’t just another monthly bill.

It’s one of the most important financial safety nets you’ll ever have.

The right coverage can protect your income, assets, family, and future.

The wrong coverage or no coverage at all can turn a manageable setback into a financial disaster.

Take a few minutes today to review your policies, identify any gaps, and make sure you’re protected against life’s unexpected events.

Your future self will thank you.